Time and labor savings

E-billing eliminates the need for OCR extraction of content, which reduces the error rate. In addition, processing times and delivery are possible in real time, which increases time efficiency.

Cost Savings

E-billing reduces postage and paper costs, as physical invoices are no longer required.

Security and Compliance

E-invoices can be transmitted digitally and securely, ensuring correct transmission and protection of your confidential data.

Transparency & Archiving

Each step of the process can be tracked precisely, ensuring greater transparency. The status and history of a transaction can be viewed at any time, and digital documents such as e-invoices are archived automatically in a space-saving manner, remain legible indefinitely, and any changes are logged.

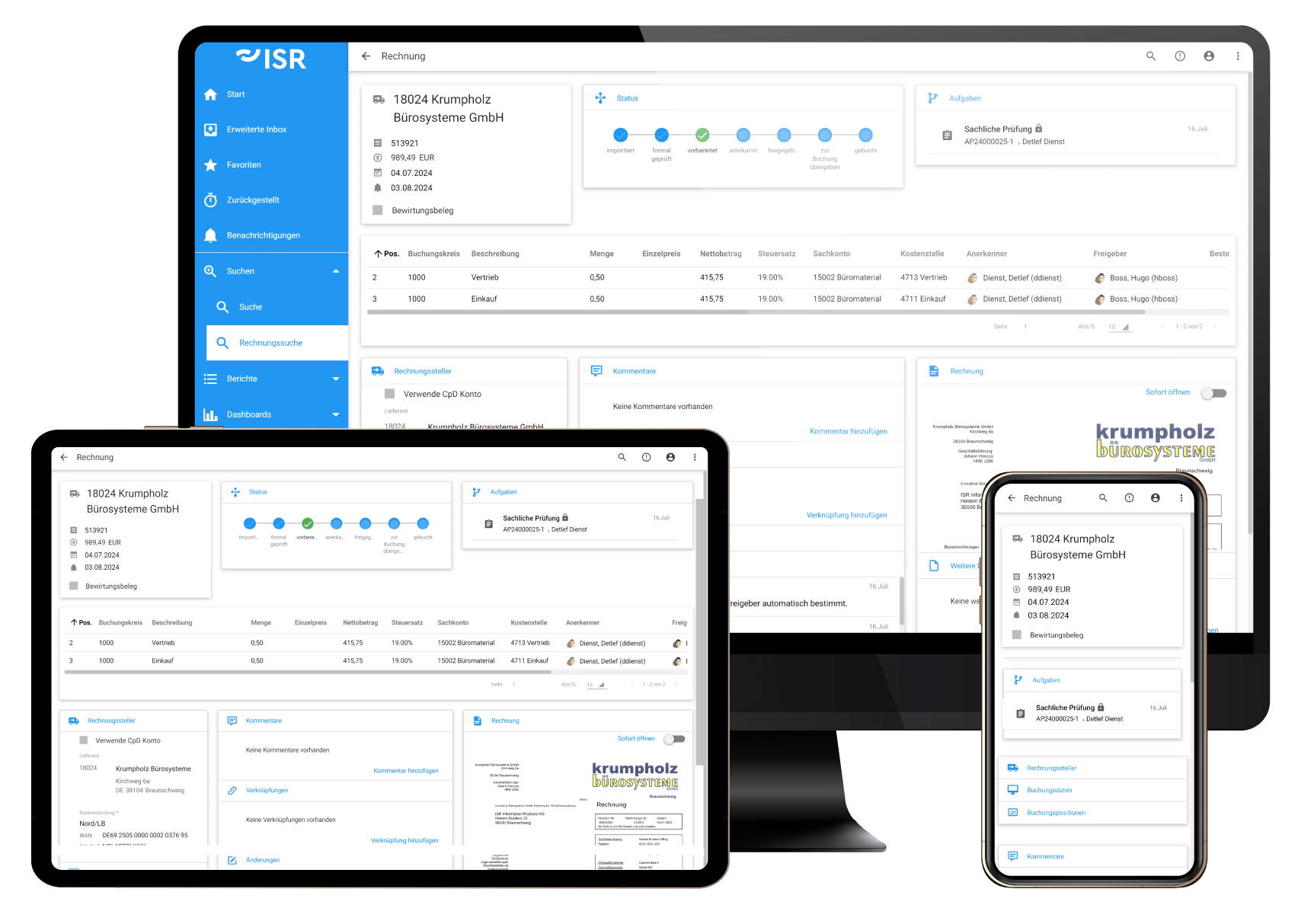

Accounts Payable Flow